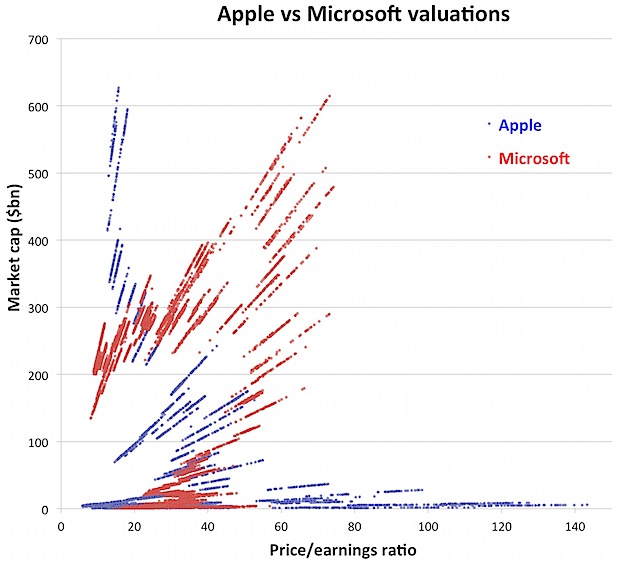

Many thanks to Ben Walsh and the Thomson Reuters data team for helping put this chart together. There’s a lot of data here, which isn’t easy to obtain: some 15,000 datapoints in all, going back as far as 1983.

The chart was inspired by this post by Nick Wingfield — the point at which Apple’s market capitalization, in nominal terms, finally exceeded the previous all-time high, which was set by Microsoft in 1999. So we went back and took the closing share price of AAPL and MSFT for every day since they went public, and plotted the market cap against the p/e ratio every day. Apple’s closing prices are in blue; Microsoft’s are in red.

The first thing to notice is the huge difference in p/e ratios at the maximum market cap. The highest AAPL point is a market cap of $627 billion, with a p/e ratio of 15.7. The highest MSFT point, by contrast, is a market cap of $615 billion, with a p/e ratio of 73.

Apple too has traded at whopping great multiples in the past — just look at that long tail of blue dots hugging the x-axis. (In fact, for the sake of clarity I truncated that axis a bit, since it goes on a lot further out than that.) But if you bought AAPL stock at a p/e of 373 you’d look pretty smart right now: the shares have gone up almost 100 times since then. Whereas, if you bought MSFT stock at a p/e of 73, you would just have ended up losing a lot of money.

If you stop looking at individual points and start looking just at the general shapes of the charts, there’s a strong positive correlation on the Microsoft datapoints, and a strong negative correlation on the Apple ones. Generally, with Microsoft, the higher the market cap the higher the p/e; whereas with Apple, the higher the market cap the lower the p/e. (Mathematically, the correlation on the Microsoft data +0.22, while the the correlation on the Apple data is -0.10.)

What this says to me is that the market in Apple shares looks a lot more rational than the market in Microsoft shares. Investors will pay huge multiples for Apple shares when the company looks cheap, but not when the company looks expensive. When Apple breaks the half-trillion barrier, that’s despite the fact that its p/e ratio is low; when Microsoft breaks that barrier, it’s because its p/e ratio is high.

So when Wingfield talks about “investor euphoria” surrounding Apple, bear in mind that the euphoria he’s talking about is very different from the kind of euphoria we saw at the height of the dot-com bubble. Apple is indeed worth a truly enormous amount of money. But investors don’t see the kind of scalability in Apple, circa 2012, that they saw in Microsoft circa 1999. Despite the fact that the global market for smartphones today is vastly greater, and growing much faster, than the global market for Windows software was in 1999.

Update: I’ve put the data here for those who want to play around with it themselves.

There are some obvious diagonal lines in the graph, which I assume come from the fact that earnings are only updated quarterly, while the price is updated daily.

Call me a pedant if you will, but shouldn’t the data eliminate the general market sentiment at each point? In 1999 we were in the dot com boom, now we’re in a rather more pessimistic situation. If possible, I’d like to see the average P/E for the market deducted from each company’s P/E before charting the relationship with Market Cap.

It’s actually a very interesting picture, and a good article too. It would say more with the alteration though… Interesting to note that since that high Microsoft has lost some 60% of its value.

The diagonal lines come from the fact that shares outstanding are only adjusted occasionally. Prices are included in both axes, so a change in price will move the point along a diagonal.

I have no dog in this hunt, financial or otherwise. Tech stocks tend to be momentum stocks, but Microsoft still has a lot to answer for. The market just doesn’t perceive it to be a growth company, and its stock has languished for a decade (http://wp.me/pJhAL-4O). Balmer must go down in history as a massively failed CEO, although it’s not at all clear that Gates didn’t get out while the getting was good.

At the same time, I wouldn’t count on Apple to have the same market perception and profitability over the long term. That’s not a dig against Apple, just an acknowledgement of the realities of tech, and the market in general.

Cash on hand:

I think one thing that needs to be in P/E charts should be (P-C) / E where C is Cash – Debt.

Apple has a high cash balance, but that’s not really being leveraged into helping them make money as their not a retail company or an insurance company and interest rates are low so it’s not really part of their float. This can make P/E look high when it’s in fact not so high. Obviously the fact that Apple is not paying dividends matters, but if you bought the whole company, you could pay a big dividend without too negatively impacting future growth potential.

@Curmudgeon

Balmer may not have been great, but I think the fact that you would’ve gotten modest returns to this point owning Microsoft at all but the peak speaks to not exaggerate the point.

Obviously it’s been a big fall, but if you bought in the post-crash high at around 35 in 2007 and owned it now you’d only be down about 5-8% after dividends which isn’t so bad considering.

Add time dimension: It would be nice if clicking one of the lines made all the others fade (like in the Gapminder plots) except for the corresponding line (same date) of the other company.

Regarding Apple’s cash pile, over the next 12 to 18 months we’re going to see a lot more over-leveraged companies in trouble; companies with cash in the bank are going to be not just the survivors, but the group that takes advantage of the fallout IMO.

@curmudgeon If you think of Microsoft as an IBM type dinosaur, and Apple as a kind of Sony mammal it helps understand their relative successes. Microsoft just wants to dominate, to be the biggest there is in anything it can see; Apple on the other hand looks for the gaps and expands them with new models, new ideas, and exciting offerings. Dinosaurs go extinct. Mammals evolve.

The big take home is the hole in the middle (esp for MS). The market never valued the stocks properly, which tells you something important about why economics doesn’t work.

FS – Sorry to intrude here but I am sure you are aware that your Reuters blog site has been offline for weeks now. Had no other way to communicate this to you, or to them.

Felix – thanks for this terrific chart, and interesting article. Any chance that you could make the data available (e.g., as a Google Docs spreadsheet) so we could play with it ourselves?

JG, that’s an interesting idea, except that the cash should be creating revenue also (interest). Maybe you could subtract that out.

One big reason Apple’s P/e trades a much lower multiple than you might expect is due to its reliance on trends. It has gotten a lot of mileage out of “being the current hawtness”, particularly among yuppies, for about a decade now. While that has been a real triumph of commercial acumen, it isn’t nearly as stable/reliable/projectable as say Microsoft’s enterprise business.

That business for Microsoft will be there for a long long time, and if it erodes it will only do so slowly. Meanwhile Apple could easily fall to just a fraction of the smartphone or tablet market in just a few product cycles.

@Measure for Measure: It’s actually because earnings are only updated once a quarter. You can think of P/E as share price/EPS, but also as market cap/earnings. If you plot market cap against P/E during a quarter, the denominator in P/E is fixed, so all the observations line up with a slope of 1/earnings. I’ve created a version of the chart where all observations for each quarter are collapsed by taking an average of daily market caps and an average P/E (lengthier explanation).

-0.10 is not strong negative correlation. Somewhat negatively correlated but not “strong”.

I fear the Reuters Blog is broken again – I can’t post a comment on your Bernanke piece, or even on your ‘Back from Holiday’ piece… you’d think they could sort out a simple blog site! (The blog posts aren’t simple – just the coding needed to create a blog (see WordPress for instance).

The Reuters site is now making it very difficult to even login. To be honest, I can’t be arsed going through all that rigmarole again. Why can’t they just sort it out with an easy solution? Any problems they had were probably from poor coding anyway – which probably haven’t been fixed. Like all reactions to security issues, the response is another layer of security, not addressing the core issue. And that goes for Politics, Nations, Foreign Policy, Economics, and Blogging too! lol!

I see nobody is commenting on the Reuters site – have they closed the comments section because they want to suck in advertising revenue from the Republican Party in the election run up and don’t want people making fun of Romney or his ideas there I wonder?

I have followed both Microsoft and Apple since 1985 and used mostly Microsoft products. The chart is telling me that the stock market is pricing Microsoft as a technology company and Apple as a design company. This means for Apple’s market cap to reach higher than it is now, its PE will go lower. My guess is that the peak market cap for AAPL will occur when its PE is similar to the 10 year average PE of companies like BAC, GS, WFC, or TWX.

Great chart!!! I have never considered AAPL and MSFT to be true competitors or technical equivalents but don’t know how to explain their subtle differences. And this chart truly help me to understand how each companies are seen by society and by the stock market.

Spyware RemovalA_B_C_NX

It is not my first time to go to see this web site, i am browsing this site dailly and obtain

good data from here every day.

I am regular reader, how are you everybody? This piece of writing posted at this website is actually good.

Link exchange is nothing else except it is just placing the other person’s webpage link on your page at appropriate place and other person will also do same in favor of you.

First of all I want to say awesome blog! I had a quick question which I’d like to ask if you do not mind. I was curious to find out how you center yourself and clear your head before writing. I have had difficulty clearing my thoughts in getting my ideas out. I do enjoy writing however it just seems like the first 10 to 15 minutes tend to be lost simply just trying to figure out how to begin. Any suggestions or hints? Thank you!

Now I am ready to do my breakfast, once having my breakfast

coming over again to read other news.

Also visit my website :: free ipad 3

Have you ever considered creating an ebook or guest

authoring on other sites? I have a blog based on the same information you discuss and would love to have you share some stories/information.

I know my viewers would value your work. If you’re even remotely interested, feel free to send me an email.

A person necessarily assist to make seriously posts

I might state. That is the very first time I frequented

your web page and up to now? I surprised with the analysis you made to create this actual post amazing.

Magnificent task!

With havin so much content do you ever run into any issues of plagorism or copyright

violation? My site has a lot of exclusive content I’ve either written myself or outsourced but it seems a lot of it is popping it up all over the internet without my agreement. Do you know any techniques to help protect against content from being stolen? I’d genuinely appreciate it.