Yves Smith at Naked Capitalism submits:

Frankly, this is pathetic. If Bernanke and his minions can’t take the heat of some well-deserved criticism from the highly-regarded Martin Wolf of the Financial Times, they don’t belong in public service.

To recap: yesterday, Wolf issued a stinging rebuke of Bernanke’s conduct on the Financial Times editorial page, in “Central banks should not rescue fools.”

Wolf first took aim at Bernanke for giving all appearances of having submitted to political pressure. The Fed chairman not only met with Henry Paulson and Senate Banking Committee chairman Christopher Dodd, but then appeared jointly with them. The Federal Reserve is supposed to be independent, yet as Wolf put it, “This showed Mr Bernanke as a performer in a political circus.”

His next criticism:

Policymakers must distinguish two objectives: the first is macroeconomic stability; the second is a sound financial system. These are not the same thing. Policymakers must not only distinguish these objectives, but be seen to do so. The Federal Reserve failed to do this when it issued statements, on prospects for the economy and on emergency lending, on August 17. This unavoidably – and undesirably – confused the two goals.

Enter Greg Ip of the Wall Street Journal. Ip is widely considered to be a preferred, if not the preferred, outlet for informal communications from the Fed.

Now as of this hour, the WSJ first page‘s “What’s News” column has this summary of an article by Ip as its lead item:

Bernanke is showing signs of a break with Greenspan by distinguishing between the Fed’s two main roles of maintaining financial and economic stability.

This is a direct rebuttal to Wolf, editorializtion masquerading as news.

It gets worse. From the article “Bernanke Breaks Greenspan Mold,” by Ip:

To Mr. Greenspan, market confidence and the economy’s growth prospects were so intertwined as to make the Fed’s two duties almost inseparable. He cut rates after the 1987 stock-market crash and the near-collapse of hedge fund Long-Term Capital Management in 1998 to prevent investor reluctance to take risks from undermining the nation’s economic growth.

By contrast, Mr. Bernanke distinguishes between the central bank’s two functions. So, on Aug. 17, the Fed cut the interest rate and lengthened the term on loans to banks from its little-used discount window in hopes banks would use the window — or at least the knowledge it was available — to lend to solid borrowers having trouble getting credit amidst the market turmoil. The action was aimed at restoring the normal functioning of disrupted credit markets, not primarily at boosting growth.

Ip should be too seasoned a Fed watcher to buy this bunk (although some have suggested he serves as a scribe for the Fed). And it goes without saying that the existence of Wolf’s piece is never mentioned.

The discount window was not an effective mechanism for dealing with the seize up in the money markets, which was where the crisis lay. That problem resulted from a repudiation of asset backed commercial paper, which potential buyers feared might be tainted by subprime exposure. Many of the issuers who couldn’t roll it were either corporations or special purpose entities that had no access to the bank discount window. Thus Bernanke’s move was no remedy.

As we said at the time, the important act that day was not the discount rate cut, which was merely symbolic, but the Bernanke commitment via Dodd, that the Fed stood ready to act, which traders have taken as a promise that a Fed funds rate cut is soon coming. In fact, our reaction on August 17 was that Bernanke’s actions showed him to be the true heir of “Greenspan put” Al. But Ip would have us believe otherwise.

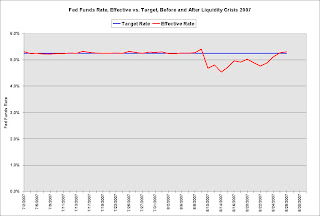

Our dim view is further confirmed by the fact that the Fed has allowed the Fed funds rate to trade below its target levels for most of the last two weeks (chart courtesy Calculated Risk):

Calculated Risk notes that this de facto easing is much less than during the 9/11 period.

So we can either believe Ip is an idiot or he is so loyal to his Fed sources that he will take a story line from them and faithfully write it up. I’m inclined towards the latter view. And if true, that is even more discouraging that what Wolf told us yesterday.

to join after the body does not stimulate your skin soft, soft comfort UP. Fashion can not without

presence in Winter.and ugg boots have many series.such as:

to join after the body does not stimulate your skin soft, soft comfort UP. Fashion can not without

presence in Winter.and ugg boots have many series.such as:

we know winter is very cold,we began ? We professional supply

,

,

,

,

,

online,this winter the best way to keep your feet warm is to get a pair of ugg Boots.