Should we care about what the markets did on Tuesday? The news made the front page of just about every newspaper in the world, so it’s clearly important, right?

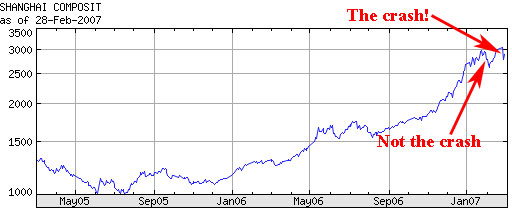

Well, let’s keep things in perspective. Here’s a stock chart for the Shanghai Composite, which crashed on Tuesday and brought the world down with it:

See the crash? It’s that little blip which sent the index tumbling all the way back to where it was in mid-January: the Composite is still up 7.7% since the beginning of 2007, and up 148% since the beginning of 2006.

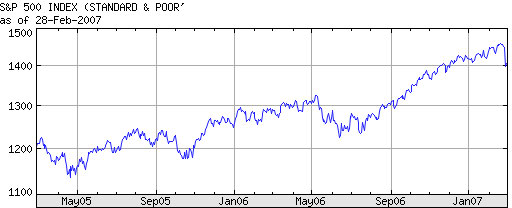

Now, here’s the S&P 500 over the same timeframe:

Clearly, the S&P 500 hasn’t more than doubled in the past year. But equally clearly it’s recovered more than once from much bigger falls than it saw on Tuesday. The only remotely unique thing about what happened on Tuesday is that it happened in one day, rather than happening over the course of a week or two.

The problem is that because of the news cycle, things which happen quickly are more newsworthy than more important things which happen slowly. So a big fall in the stock market over the course of one day makes front pages around the world — and if you’re going to make a big deal out of why the stock market fell, then you’re going to have to come up with some kind of reason for it.

Enter the bears. You want an explanation for why the market went down? Econobloggers from Roubini to Ritholtz to Baker have been telling you for months why the market should be going down! It all starts with the housing market: homebuilders have stopped building homes, which means that manufacturers have had to stop making stuff for all those homes, and that both the building and manufacturing industries are in recession. And given the huge rise in employment in those industries of late, it stands to reason that there’s going to be a pretty big fall in employment in those industries pretty soon. Meanwhile, suppliers of mortgages have stopped writing the crazy mortgages that were driving the housing industry, which means that it’s harder to buy a house than it used to be, and that prices have stopped rising and in fact have started falling in many areas. Because those crazy mortgages are no longer available, people who have them can’t refinance, and are defaulting in unprecedented numbers — which means their homes coming back on the market, which only serves to make the broader housing market worse. And high default rates also hit mortgage-backed securities, which make up a large chunk of the US bond market, raising fears of a credit crunch. Add it all up, and you get Recession — which is more than enough reason for a market “priced for perfection” to fall — and fall a lot.

Now, this story really hasn’t changed over the past 6 months. The same people are telling the same story that they have been telling for a long time — and, truth be told, those of them who made forecasts for when the market and the economy would turn south have seen those dates come and go. Now, it’s entirely possible that, finally, their time has come — that February 27 will be seen, in retrospect, to be the beginning of a nasty bear market where spreads widen out, credit contracts, stocks fall, and the economy slides into recession. But it’s way, way too early to tell. But at least the story makes for a good explanation for the fall in global stock markets. (And remember, journalists love compelling explanations for such things.)

In truth, one-day movements in the stock market are nearly always meaningless. OK, there was the crash of 1929, which was hugely important. And the crash of 1987, which was of minor importance. But as a general rule, anybody who tries to extrapolate a general stock-market direction from what the market does in one given day is on a fool’s errand. So the market might go down over the next few months, and it might go up over the next few months. But either way, what happened on Tuesday is not going to be particularly important in terms of the bigger move.

And what about the economy? Are we headed for recession or not? Here, the important market players all seem to be on more or less the same page. Ask Wall Street economists, or Fed governors, or the US Treasury what they think, and they’ll nearly all say that the economy might be slowing down, but they don’t see much risk of a recession or any other type of “hard landing”. On the other hand, there seems to be an equally compelling unanimity among newspaper columnists and econobloggers that the markets are delusional and cruising for a nasty crash.

Now it’s true that market economists, and the market in general, never seem to see a crash coming until it’s too late — so the fact that they don’t think there’s going to be one is hardly reassuring. Quite the opposite, in fact. On the other hand, no one ever made money by listening to macroeconomists.

As Brad DeLong says, “the macroeconomic outlook rarely changes suddenly”. Whatever is true today was true last week. So if you thought things were going fine last week, the release of a durable goods report and a one-day blip in the markets should not be enough to change your mind. Similarly, if you thought markets were overpriced last week, you should resist the temptation to believe that the markets have now suddenly come around to your way of thinking.

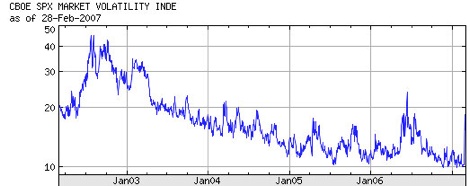

One last chart for you:

That’s the VIX volatility index. It’s spiked up — last at 16, from typical levels between 10 and 12 of late. But the spike looks bigger because Yahoo charts make their y-axes logarithmic. We’re still a long way from the Great Unwind that so many people fear.

Hope that this is just a correction. Globalisation has led to ripple effect which happens in one part of the world to affect others as well.

Felix — I would never tell the market it should be going down; Rather, I attempt to alert people to the risks ignored or glossed over by Wall Street salespeople, cheerleading politicians, and the Fed (who tend towards happy talk).

The market will do what it does, regardless of what you and I say. However, we can recognize that the Business cycle has not been repealed, that significant risk exists, and that the economy is cooling.

This realistic perspective apparently is perceived as hopelessly curmudgeonly by many people.